Table Of Content

On the other hand, a homeowner who is refinancing may opt for a loan with a shorter repayment period, like 15 years. This is another common mortgage term that allows the borrower to save money by paying less total interest. However, monthly payments are higher on 15-year mortgages than 30-year ones, so it can be more of a stretch for the household budget, especially for first-time homebuyers. Amortization is the process of gradually paying off a debt through a series of fixed, periodic payments over an agreed upon term. The payment consists of both interest on the debt and the principal on the loan borrowed. At first, more of the monthly payment will go toward the interest.

What’s a homeowners insurance premium?

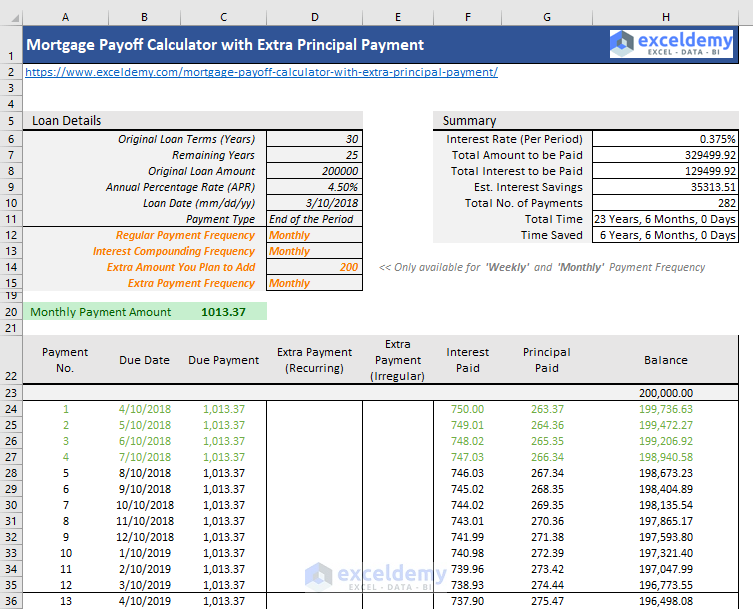

If you buy a home with a loan for $200,000 at 4.33 percent your monthly payment on a 30-year loan would be $993.27, and you would pay $157,576.91 in interest. If your interest rate was only 1% higher, your payment would increase to $1,114.34, and you would pay $201,161.76 in interest. The mortgage calculator estimates a payment that includes principal, interest, taxes and insurance payment — also known as a PITI payment. These four key components help you estimate the total cost of homeownership. A mortgage payment calculator helps you determine how much you will need to pay each month to pay off your mortgage loan by a specific date. An extra payment is when you make a payment in addition to your regular monthly mortgage payment.

Are property taxes included in mortgage payments?

This 20% is the equity that you will immediately own in the house, which gives you certain advantages if you later decide to refinance the mortgage or sell the house in the future. One of the ways that you can make extra payments is through the bi-weekly payment plan that we mentioned earlier. To decrease the amount of interest you pay and to shorten the time during which you are expected to pay off your mortgage, you can make extra payments on your mortgage. These extra payments will decrease the principal left to repay and the interest amount charged on it going forward.

Monthly payment: What’s behind the numbers used in our mortgage payment calculator?

The DTI ratio looks at the percentage of your gross monthly income that goes towards monthly debt repayments. For example, if your monthly income is $5,000 and $2,000 goes towards debt payments, your DTI ratio is 40% ($2,000/$5,000). On the other hand, if you put at least 10%, you only have to pay MIP for 11 years. This means that after 11 years, your monthly payment will be smaller as it will not include MIP.

How Do You Apply for a Mortgage?

New Mexico Mortgage Calculator - The Motley Fool

New Mexico Mortgage Calculator.

Posted: Thu, 07 Mar 2024 08:00:00 GMT [source]

Calculating your mortgage payment on your FHA loan is similar to calculating the mortgage payment on a regular mortgage. You will need the house’s price, the down payment, the mortgage rate, and the mortgage term for an estimation of your monthly payments. The biggest difference between the two stands in the mortgage insurance that you will have to pay if you put a down payment smaller than 20% of the house’s price. As a home buyer, you’ll want to have a certain level of comfort in understanding your monthly mortgage payments.

Calculator assumption: 20% down payment

These taxes generally pay for services such as road repairs and maintenance, school district budgets and county general services. This is based on our recommendation that your total monthly spend for your monthly payment and other debts should not exceed 36% of your monthly income. Interest rates vary depending on the type of mortgage you choose. See the differences and how they can impact your monthly payment. This mortgage payment calculator assumes that you’re buying a single-family home as your primary residence. An important part of the home buying process for buyers is knowing how much house they can afford.

How long are mortgage terms?

The actual amount you pay depends on several factors including the assessed value of your home and local tax rates. LendingTree data show that comparing mortgage quotes from three to five lenders can save you big on your monthly payments and interest charges over your loan term. VA Funding Fee – Borrowers of VA loans will typically have to pay around 1.4% to 3.6% of the amount borrowed as a VA funding fee. The exact rate depends on the specific VA loan you are applying for, whether you make a down payment or not, and whether you have used a VA loan in the past. The VA Funding Fee can either be paid upfront or you can choose to roll over the amount into the loan.

Honestly, the situation is so bleak, people may need to consider other countries. While it depends on your state, county and municipality, in general, property taxes are calculated as a percentage of your home’s value and billed to you once a year. In some areas, your home is reassessed each year, while in others it can be as long as every five years.

VA Mortgage Payments

The length of your mortgage terms dictates (in part) how much you’ll pay each month—the longer your term, the lower your monthly payment. Keep in mind, however, that just because you can afford a house on paper doesn’t mean your budget can actually handle the payments. Beyond the factors your bank considers when pre-approving you for a mortgage amount, consider how much money you’ll have on-hand after you make the down payment. It’s best to have at least three months of payments in savings in case you experience financial hardship. Using a mortgage calculator will give you a rough estimate of what you can expect to pay for homes in different locations at different price points.

For example, if you live in a flood zone or a state that’s regularly impacted by hurricanes, you may be required to buy additional coverage that protects your home in the event of a flood. If you live near a forest area, additional hazard insurance may be required to protect against wildfires. A down payment of 20% or more will get you the best interest rates and the most loan options.

A mortgage discount point calculator can help you determine if this is worth it for you. Down payment & closing costsNerdWallet's ratings are determined by our editorial team. The scoring formula takes into account the type of card being reviewed (such as cash back, travel or balance transfer) and the card's rates, fees, rewards and other features. Remember, your monthly house payment includes more than just repaying the amount you borrowed to purchase the home.

This is based on the loan amount (the home price minus your down payment), interest rate and term length you entered. What if you’re not looking to move to a new place, but instead looking to refinance your current home? The first question a refinance calculator will ask you is what your goal is with a refinance. For example, you might wish to lower your existing loan payment, pay off your mortgage faster or take cash out. There are a few types of mortgage calculators that can prove helpful depending on your situation. Let’s go over the basics on each of them, before digging a little deeper into the information you’ll need to make the most use of each calculator.

If you’re new to buying a home, you may not realize all the costs that go into it. In addition to your loan balance and interest, you’ll have to consider property taxes, homeowners insurance, PMI and more. If you’re new to homeownership, you may not realize that the loan amount isn’t the only factor to consider when determining how to calculate a mortgage payment. Let’s look at how mortgage payment calculators break down your monthly mortgage expenses. The “taxes” portion of your mortgage payment refers to your property taxes. The amount you pay in property taxes is based on a percentage of your property value, which can change from year to year.

Not all loan programs are available in all states for all loan amounts. Interest rates and program terms are subject to change without notice. It includes both your down payment and the total amount (principal) of your mortgage loan. And when you’re searching for a mortgage, the home price is the most easily adjustable factor. For example, you can’t negotiate on the property taxes in your state, but you can always try to negotiate a lower price on your home. Lenders typically require you to purchase homeowners insurance when you have a mortgage.

Therefore, the decision comes down to you, whether you are willing to take on more debt for a pricier home or keep debt low and sacrifice on the home you purchase. The most common mortgage terms are 30-year and 15-year mortgages. With a 30-year mortgage term, all else the same, your monthly mortgage payment is going to be lower than with a 15-year mortgage term. This happens because, with a 15-year term, you will have to pay the same amount in a shorter period of time, which is why the mortgage payments will have to be larger.

This typically happens at the end of your term unless you make extra payments. In exchange for giving you a loan, your lender will charge you interest on the total amount you borrow. For instance, a 4% interest rate means you’ll pay 4% on the total loan balance until the mortgage is paid off. These loans have interest rates that reset at specific intervals.

No comments:

Post a Comment